Sell Your Mortgage Note in San Francisco

The Bay Area produces some of the highest-value seller-financed notes in the country. From San Francisco proper to Oakland, Silicon Valley, and Marin County — our team can review your note and tell you exactly what it's worth. No pressure, no obligation. Call 954-466-7111 or request a free review below.

San Francisco, California

San Francisco Sell Mortgage Notes — Seller-Financed & Owner-Financed Notes — What You Need to Know

San Francisco and the broader Bay Area — including Alameda, Contra Costa, Marin, San Mateo, and Santa Clara counties — produce some of the highest-value seller-financed notes in the country. California ranks 3rd in the nation with over 7,000 seller financed notes annually, and the Bay Area's extreme property values push note sizes well above the national average. Jumbo seller-financed notes are common here, along with tech worker and investor seller-financed transactions, estate sales from longtime owners, and multi-family and mixed-use properties. California requires a Seller Financing Disclosure Statement (Cal. Civ. Code §2956) for all seller-financed transactions involving 1–4 residential units. Note holders ready to sell mortgage note San Francisco real estate secures should gather your mortgage or deed of trust (depending on your state) before contacting our team for a review.

How to Sell Your San Francisco Mortgage Note in 4 Steps

Gather Your Documents

Promissory Note, your mortgage or deed of trust (depending on your state), and the closing statement from the original sale. Call 954-466-7111 if you need help locating them.

Request a Free Review

Submit your note details below for a free, no-obligation review. Click HERE to Request a FREE Note Review

Review Your Offer

Compare the purchase price and structure — full purchase, partial sale, or split buyout. No pressure to decide immediately.

Close & Get Paid

We handle underwriting, title check, and closing costs. Funds are wired directly to your bank account in 3–5 weeks when all documents are received and title is clear.

We Buy Mortgage Notes Throughout San Francisco & the Bay Area

Sell Your Mortgage Note in San Francisco County

San Francisco proper generates high-value residential and multi-family seller-financed notes. The city's tech-era transactions and extreme property values mean notes secured by San Francisco real estate are frequently well above the national average note size.

Sell Your Mortgage Note in Alameda County

Oakland, Berkeley, and Fremont form one of the Bay Area's most active investor markets. Alameda County produces significant seller-financed note volume across residential and investment properties.

Sell Your Mortgage Note in Silicon Valley (Santa Clara & San Mateo)

San Jose, Palo Alto, and Menlo Park generate high-value notes, often tied to tech employee seller financing. Santa Clara and San Mateo counties consistently produce some of the largest seller-financed note balances in California.

Sell Your Mortgage Note in Marin & Contra Costa Counties

Marin County — Mill Valley, San Rafael — and Contra Costa County are affluent markets where estate and probate notes are common. Longtime property owners in these counties frequently hold seller-financed notes created decades ago.

Don't see your area? We buy notes throughout all of California. Call 954-466-7111 or submit your note details below.

Request a FREE Note ReviewFree — No Obligation

Ready to Find Out What Your Bay Area Note Is Worth?

Our team reviews your note and responds within one business day — no fees, no pressure, no obligation.

What Note Buyers Are Actually Evaluating

When our team reviews your note, here is what we are looking at — and how each factor affects your offer:

The creditworthiness of the borrower making payments on your note. A stronger credit score signals lower default risk and directly improves your offer. Even a rough credit range — strong, fair, or weak — helps us evaluate the note before a full review.

The larger the original down payment, the more skin in the game the borrower had from day one. A 10%+ down payment is a strong signal of borrower commitment and significantly reduces default risk — making your note more attractive to note buyers.

The remaining loan balance divided by the current property value. Lower LTV means more equity in the property — the single biggest pricing factor. The Bay Area's high appreciation often produces favorable LTV ratios.

How many consecutive on-time payments the borrower has made. 12+ months of clean payment history significantly improves your offer.

First position notes are far easier to sell than second position notes. A second lien means another lender has priority claim on the property — that adds risk and typically reduces the offer significantly.

Higher interest rates on your note generally mean a better yield — and therefore a better offer — for the note buyer.

Single-family residential notes in desirable markets command better pricing than rural land or commercial notes. High-demand Bay Area markets like San Francisco, Oakland, and the Peninsula are favorable.

Deed of trust states with faster non-judicial foreclosure timelines are generally more favorable for note buyers — and that can translate into a slightly better offer for you.

How long ago the note was created. Very new notes with under 6 months of payment history are harder to price — but once seasoning builds, age alone is rarely a deciding factor.

Whether the property is owner-occupied, tenant-occupied, or vacant. Owner-occupied is the preferred scenario, but tenant-occupied notes are still purchasable. Vacant properties carry the most risk.

The price the property sold for when the note was created. Helps verify the transaction was arm's length and the original LTV was reasonable — useful context but rarely changes the offer on its own.

Note balances are typically $100,000 and above given Bay Area property values, though smaller notes are still reviewed. Very small balances can be harder to sell because transaction costs consume more of the yield.

Whether the note is fully amortizing, interest-only, or has a balloon payment. Standard amortizing notes are the easiest to price. Balloon, interest-only, and all-inclusive trust deed (AITD/wraparound) structures are purchasable but require additional analysis.

Want to know exactly what documents we need? See our full Note Documents Checklist for a step-by-step breakdown of everything to gather before your review. For more on how note pricing works, visit our Moxxie blog.

Seller-Financed Notes Go by Many Names in San Francisco

Whether you call it a seller financed note, an owner financed note, or a private mortgage note — it's the same instrument and we buy them all. Bay Area note holders also hold deeds of trust, all-inclusive trust deeds (AITDs/wraparounds), and land contracts. We buy all types.

Owner-Financed Mortgage Note

Same as a seller-financed note — the property seller acts as the bank, accepting monthly payments directly. We buy owner-financed notes throughout San Francisco and all of California.

All-Inclusive Trust Deed (AITD / Wraparound)

A wraparound financing structure common in high-value Bay Area transactions, where the seller-financed note "wraps" around an existing underlying loan. We review and purchase AITDs regularly.

We Buy Deeds of Trust & Land Contracts

Sell your deed of trust or land contract for a lump sum. We buy all types of seller-financed instruments in San Francisco — deeds of trust, all-inclusive trust deeds, private mortgage notes, and land installment contracts.

Why San Francisco Bay Area Note Holders Choose Moxxie Asset Group

Selling a mortgage note is a one-time decision for most note holders. Our team is experienced with California deed of trust notes — including the high-value Bay Area market — and focused on giving you an honest, no-pressure review so you can make the best decision for your situation.

We Know Bay Area Notes

Our team understands the local market, the deed of trust structure used in this state, and what makes a high-value Bay Area note trade at full value. We review San Francisco notes regularly and can give you an honest, informed assessment — not a lowball offer.

Honest, No-Pressure Process

Our team reviews your note and responds within one business day. We walk you through exactly how we arrived at our offer — no mystery pricing, no bait-and-switch, no pressure. If a full sale isn't right for you, we'll tell you. A partial note purchase may be a better fit.

Free Review — No Fees, Ever

There are no upfront fees, no application costs, and no obligation attached to your review. We cover our costs at closing — only if you decide to sell. Call 954-466-7111 or request your free review below.

Request a FREE Note ReviewCalifornia Mortgage Note Law — What San Francisco Note Holders Need to Know

California Note Law Summary

California uses deed of trust instruments (not mortgages) and a non-judicial trustee sale foreclosure process — typically ~120 days under Civil Code §2924. California's one-action rule (CCP §726) requires lenders to pursue the security (the property) before any other remedy, and strong anti-deficiency protections apply to purchase-money notes (CCP §580b). The Seller Financing Disclosure Statement (Cal. Civ. Code §2956) is required for all seller-financed 1–4 unit residential transactions. Bay Area note assignments are recorded with the applicable county recorder — San Francisco, Alameda, Contra Costa, Marin, San Mateo, or Santa Clara.

Documents Required to Transfer Your Note

- Original promissory note (wet-ink)

- Recorded Deed of Trust assignment

- Allonge or endorsement of the note

- Settlement statement / HUD-1 from original closing

- Payment history records

- Title insurance policy

This information is provided for educational purposes only and does not constitute legal advice. Consult a qualified attorney for guidance specific to your situation. Source: California Statutes.

San Francisco Mortgage Note Holder FAQ

Can I sell my seller-financed mortgage note in San Francisco?

Yes. San Francisco and the broader Bay Area produce some of the highest-value seller-financed notes in the country. Whether your note is on a San Francisco County property, an Oakland investment, or a Silicon Valley home, Moxxie Asset Group can review it at no cost. California uses deed of trust instruments — transferring your note requires an endorsed promissory note and a recorded Assignment of Deed of Trust.

Is California a mortgage or deed of trust state?

California is a deed of trust state. Lenders use deeds of trust rather than mortgages for seller-financed transactions. This means non-judicial foreclosure applies under CA Civil Code §2924 — typically around 120 days — which makes California notes attractive to buyers. The one-action rule (CCP §726) and anti-deficiency protections (CCP §580b) are also key factors in Bay Area note valuation.

What documents do I need to sell my San Francisco mortgage note?

To get started, gather your deed of trust (California does not use mortgages), the original promissory note, your closing statement or HUD-1, and payment history. A title insurance policy is helpful but not required to begin your review. Our team can tell you what your Bay Area note is worth with just the basics. See our full checklist at /what-documents-do-i-need-to-sell-my-mortgage-note.

Real Feedback From Real People

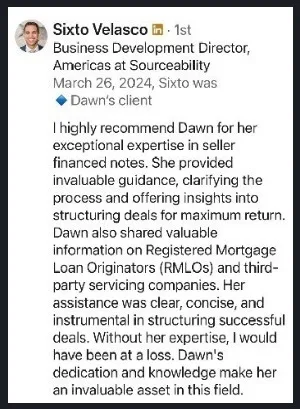

“I highly recommend Dawn for her exceptional expertise in seller financed notes. She provided invaluable guidance, clarifying the process and offering insights into structuring deals for maximum return. Her assistance was clear, concise, and instrumental in structuring successful deals.”

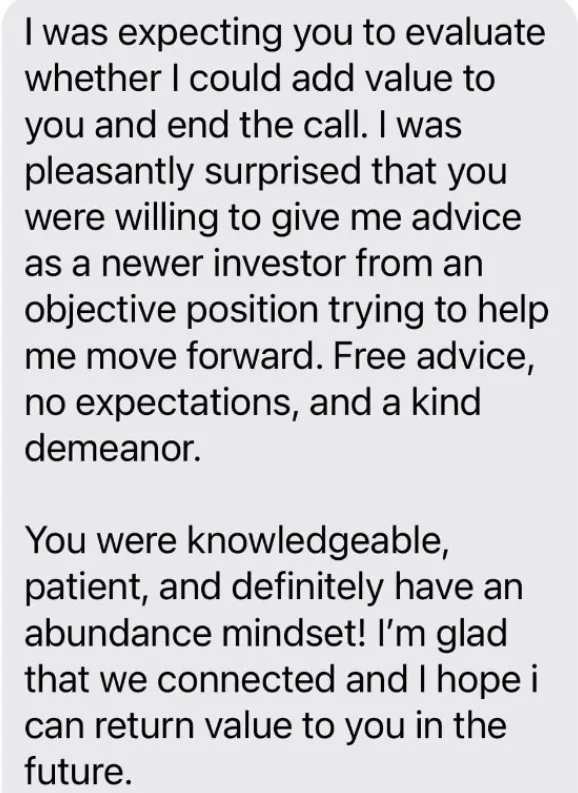

“I was pleasantly surprised that you were willing to give me advice as a newer investor from an objective position trying to help me move forward. Free advice, no expectations, and a kind demeanor. You were knowledgeable, patient, and definitely have an abundance mindset!”

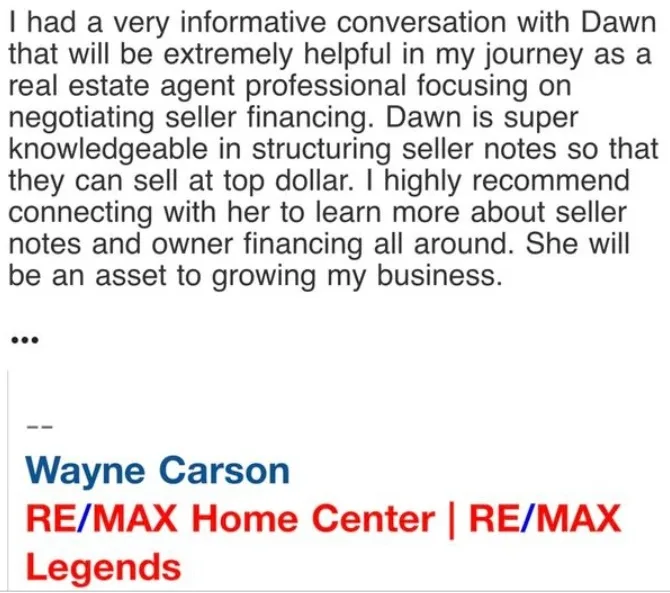

“I had a very informative conversation with Dawn that will be extremely helpful in my journey as a real estate agent focusing on seller financing. Dawn is super knowledgeable in structuring seller notes so they can sell at top dollar. I highly recommend connecting with her.”

Find Out What Your San Francisco Note Is Worth

Share a few details and we'll get back to you with a no-obligation review. Easy, free, confidential, and no commitment required.

Prefer to talk? Call us at 954-466-7111

No pressure or obligation offer · We Buy Notes Nationwide · Sell all or part of your note · Response usually within 1–3 business days