How to Sell a Mortgage Note —

A Complete Step-by-Step Guide

If you're holding a seller-financed or owner-financed mortgage note and want to convert those future payments into a lump sum of cash, here is exactly how the process works — from your first call to funding.

What Is a Seller-Financed Mortgage Note?

A seller-financed mortgage note — also called an owner-financed note or private mortgage note — is a legal document created when a property seller agrees to finance the buyer's purchase directly instead of requiring a bank loan. The buyer signs a promissory note promising to repay the seller over time, and the note is secured by a mortgage or deed of trust recorded against the property.

As the note holder, you receive monthly payments just like a bank would. But unlike a bank, you can sell that stream of future payments — in whole or in part — to a mortgage note buyer for a lump sum of cash today.

Before you begin: gather your mortgage or deed of trust (depending on your state), along with your payment history and original closing documents. Having these ready significantly speeds up your note review and offer.

Not sure which documents you need? See our complete note sale document checklist.

The Complete Process

How to Sell a Mortgage Note in 5 Steps

Most note sales close within 3–5 weeks. Here is what each step involves and what you can expect.

Request a Free Note Review

The process starts with a simple conversation. Contact a mortgage note buyer and share basic details about your note: the property address, the remaining unpaid balance, the interest rate, the monthly payment amount, and how long the borrower has been paying. You don't need to have every document in front of you at this stage.

At Moxxie Asset Group, our team reviews your note details and responds within one business day — no fees, no obligation.

- No application or upfront fee to request a review

- You can call, email, or submit through our contact form

- Our team will ask clarifying questions to understand your note

- You are under no obligation to proceed at any point

Receive Your Written Offer

Once our team has reviewed the details, we prepare a written offer. The offer reflects the present value of your future payment stream, adjusted for risk factors the note buyer evaluates during this phase.

The six factors that most affect your offer:

- Borrower credit score — the borrower's credit profile at origination signals default risk; strong credit means better pricing for you

- Down payment at origination — a substantial down payment (20–30%+) shows borrower commitment and reduces buyer risk

- Payment history & seasoning — consistent on-time payments build confidence; 24+ months of clean history commands a premium

- Remaining balance and interest rate — higher rate notes yield more to buyers

- Loan-to-value (LTV) ratio — lower LTV means less risk, better pricing

- State instrument type — deed of trust states (TX, NC, CA, GA, WA, TN, AZ, CO, OR) allow faster non-judicial foreclosure; mortgage states (FL, OH, MI) use slower judicial foreclosure, which note buyers factor into pricing

Offers are typically delivered within 3–7 business days of your initial note review. You are free to decline the offer with no cost or obligation.

Accept the Offer — Due Diligence Begins

When you accept the offer, the note buyer opens a due diligence period — typically 1 to 2 weeks. This is where they verify the note's details, the property, and the title before committing to fund.

What happens during due diligence:

- Document review — promissory note, mortgage or deed of trust, payment ledger, original closing statement

- Title search — confirms the note is in first position and the title is clear of liens

- Property valuation — a BPO (broker price opinion) or appraisal confirms current market value and LTV

- Borrower credit pull — the note buyer will pull the borrower's credit report as part of underwriting. This is legally permitted: any party extending credit — or purchasing a debt instrument secured by real property — is entitled to review the borrower's credit under the Fair Credit Reporting Act (FCRA). This is standard practice in note transactions, and as the note seller, you should know this step is coming.

A common concern: many note sellers worry that their borrower will need to consent to the credit pull — or worse, that the borrower can block it. They cannot. The FCRA grants note buyers a "permissible purpose" to pull credit without the borrower's prior consent when evaluating the purchase of a credit obligation. The borrower's permission is not required, and the borrower has no legal standing to prevent it. The credit pull is a hard inquiry, which may appear on the borrower's report, but the note buyer — not you — handles that process. You do not need to notify your borrower before due diligence begins. - Payment verification — bank statements or servicing records confirm the payment history you provided

Having your documents organized and ready before this stage is the single biggest way to speed up your closing timeline. See our full document checklist to prepare.

Sign Closing Documents

Once due diligence is complete, a title company or closing attorney prepares the transfer documents. These include an assignment of note and security instrument, which legally transfers the note from you to the buyer. You review and sign — typically via electronic signature or overnight courier for wet signatures.

Your borrower will also receive a formal notice of transfer at this stage. Federal law (RESPA) requires the borrower to be notified when a note is sold or transferred. Their loan terms — interest rate, payment amount, and schedule — do not change.

- Closing documents are typically ready within 3–5 business days after due diligence clears

- Electronic signatures are accepted in most cases

- No closing costs or fees to you — the note buyer covers transaction costs

Receive Your Funds

Once signed documents are returned and recorded, your funds are wired directly to your bank account — typically within 1 to 2 business days. The total process from first contact to funded usually runs 3 to 5 weeks for a well-documented note.

- Funds arrive via wire transfer to your bank account

- No deductions or fees — you receive the agreed offer amount

- Your borrower's future payments now go to the new note holder

- You receive confirmation and copies of all transfer documents

Full Sale vs. Partial Sale — Which Is Right for You?

One of the first decisions you'll make is whether to sell the entire note or just a portion of the remaining payments. Both options follow the same process above — the difference is in how much of your payment stream you sell.

Full Sale

You sell the entire remaining payment stream for a single lump sum. Clean break — no ongoing involvement with the note or borrower.

- Largest lump sum available

- No future note management

- Best for sellers who want full liquidity

Partial Sale

You sell a defined number of future payments for a smaller lump sum. Once those payments are collected, the note reverts back to you.

- Get cash now, keep future income

- Smaller taxable event this year

- Best for sellers who want liquidity but not a full exit

Our team will walk you through both options and help you understand the pricing difference for your specific note. Learn more about how a partial note purchase works.

Free — No Obligation

Ready to Find Out What Your Note Is Worth?

Our team reviews your note details and responds within one business day — no fees, no pressure, no obligation.

What Affects the Price You'll Receive

Note buyers use a risk-adjusted discounted cash flow model to determine an offer. In plain language: they calculate what your future payments are worth in today's dollars, then adjust for the risk that payments might not come in as expected. Here's what moves that number up or down.

Borrower Credit Score

The borrower's credit profile at origination — and their demonstrated ability to pay — directly affects how a note buyer prices risk. A borrower with strong credit is seen as less likely to default, which translates to a better offer for you. Even if the credit score at origination was low, consistent on-time payments over time can offset that concern in the buyer's eyes.

Down Payment at Origination

The down payment the buyer made when the note was created is a strong indicator of commitment and equity. A borrower who put 20–30% down has real skin in the game — they are far less likely to walk away from the property. Notes originated with substantial down payments are considered lower risk and price accordingly. Low or no down payment notes carry more risk and are discounted more heavily.

Payment History & Seasoning

On-time payment history is the single biggest value driver. A note with 24+ months of consistent payments commands significantly better pricing than one with missed or late payments. Every on-time payment your borrower makes adds to your note's value.

Interest Rate

Higher interest rate notes are more valuable to buyers because they generate more yield. Owner financed notes often carry above-market interest rates — commonly 7–10% or higher — which can work in your favor when pricing.

Loan-to-Value Ratio (LTV)

LTV compares the remaining balance of the note to the current value of the property. Lower LTV means more equity cushion, which reduces the buyer's risk if the borrower ever defaults. A note with 60–70% LTV will always price better than one at 90%+.

State Instrument Type

Your state determines how the note is secured and how quickly a buyer can act if the borrower defaults. Deed of trust states (TX, NC, CA, GA, WA, TN, AZ, CO, OR) allow non-judicial foreclosure — faster and less expensive. Mortgage states (FL, OH, MI) require judicial foreclosure through the courts, which takes longer. This timeline difference is factored into pricing.

Frequently Asked Questions

How long does it take to sell a mortgage note?

Most note sales close within 3 to 5 weeks from the initial review. The timeline depends on how quickly documents are gathered, whether a property valuation is needed, and the complexity of the note. Well-documented, seasoned notes with clean payment histories typically close on the faster end.

What documents do I need to sell my mortgage note?

You will need the original promissory note, your mortgage or deed of trust (depending on your state), a payment history or ledger, and the original closing or settlement statement. Having these ready when you request a review speeds up the process. See our complete documents checklist.

Do I have to sell my entire mortgage note, or can I sell part of it?

You do not have to sell your entire note. A partial note purchase lets you sell a defined number of future payments for a lump sum today, then continue collecting the remainder. This is a good option for note holders who want cash now but still want to keep some future income stream.

What does a mortgage note buyer look for when evaluating my note?

Note buyers evaluate six primary factors: borrower credit score at origination, down payment at origination, payment history and seasoning, remaining balance and interest rate, loan-to-value (LTV) ratio, and the state's foreclosure instrument — whether the note is secured by a mortgage or a deed of trust. Notes with strong credit, a solid down payment, clean payment history, low LTV, and high interest rates typically receive the best offers.

Does my borrower need to know I'm selling the note?

Yes. Federal law (RESPA) requires that the borrower be notified when a mortgage note is sold or transferred. The borrower will receive a written notice informing them of the new payee and where to send future payments. Their loan terms — interest rate, payment amount, and schedule — do not change.

Does my borrower have to consent to a credit check during the note sale process?

No — and this is one of the most common concerns note sellers have. Under the Fair Credit Reporting Act (FCRA), any party purchasing a credit obligation secured by real property has a "permissible purpose" to pull the borrower's credit report without their prior consent. The borrower cannot block it, and you are not required to ask for their permission or notify them before due diligence begins.

What if I never pulled credit and don't have the borrower's Social Security number? This is very common in owner financed transactions — many seller-financed deals are made on a handshake, without a formal loan application or credit check. You are not required to provide the borrower's SSN. The note buyer's underwriting team handles the credit pull as part of due diligence using information they gather directly. Your job is simply to provide the note documents and payment history — not to track down personal borrower information you never collected in the first place.

What is the difference between a mortgage state and a deed of trust state?

The difference is in how the security instrument is named and how foreclosure is handled if a borrower defaults. In mortgage states like Florida, Ohio, and Michigan, the note is secured by a mortgage and foreclosure requires a court process (judicial foreclosure), which takes longer. In deed of trust states like Texas, North Carolina, California, Georgia, Washington, Tennessee, Arizona, Colorado, and Oregon, foreclosure can happen outside of court (non-judicial), which is typically faster. Note buyers price this risk into their offers.

Real Feedback From Real People

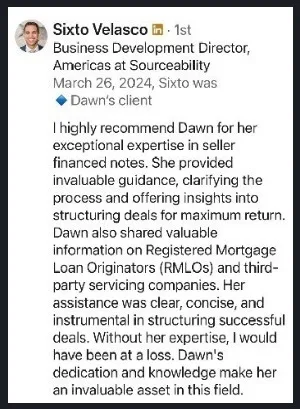

“I highly recommend Dawn for her exceptional expertise in seller financed notes. She provided invaluable guidance, clarifying the process and offering insights into structuring deals for maximum return. Her assistance was clear, concise, and instrumental in structuring successful deals.”

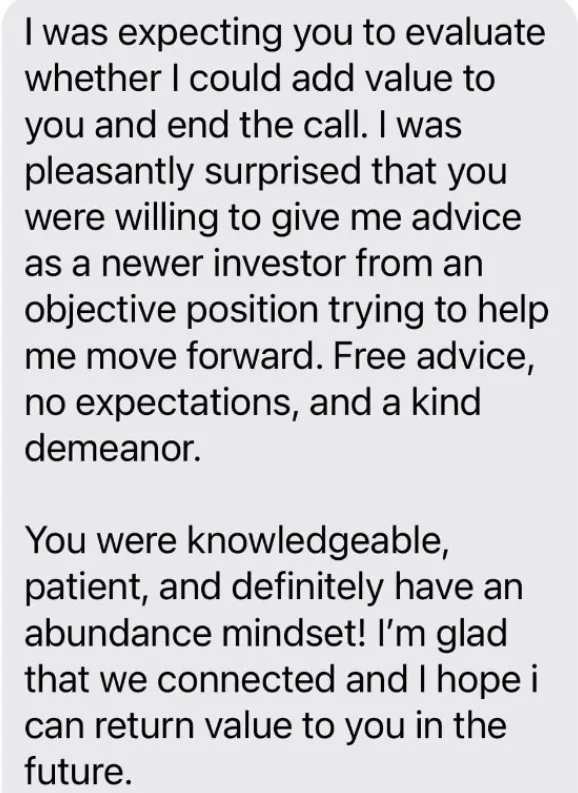

“I was pleasantly surprised that you were willing to give me advice as a newer investor from an objective position trying to help me move forward. Free advice, no expectations, and a kind demeanor. You were knowledgeable, patient, and definitely have an abundance mindset!”

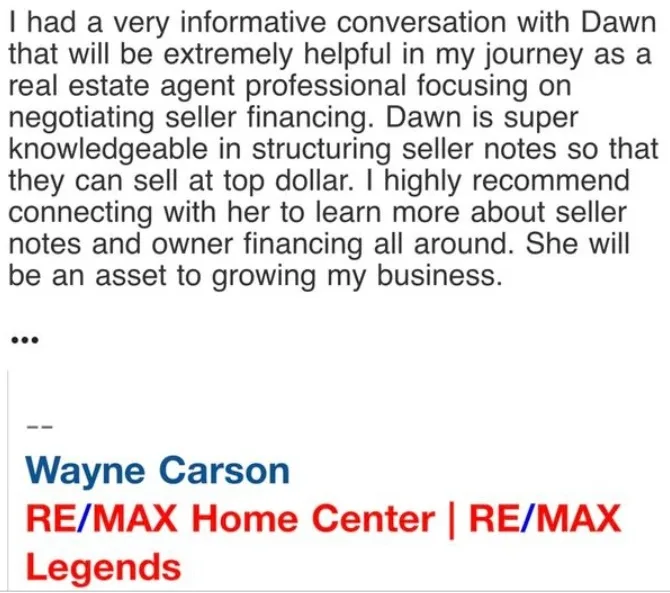

“I had a very informative conversation with Dawn that will be extremely helpful in my journey as a real estate agent focusing on seller financing. Dawn is super knowledgeable in structuring seller notes so they can sell at top dollar. I highly recommend connecting with her.”

Ready to Get Started?

Request Your Free Note Review Today

Our team reviews your note and responds within one business day — no fees, no pressure, no obligation. Whether you're ready to sell or just exploring your options, we're here to help you understand what your note is worth.