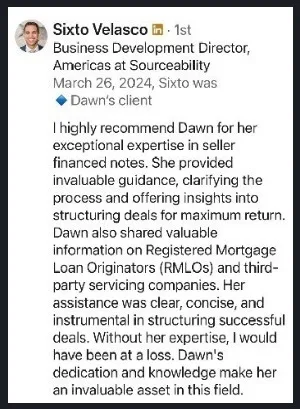

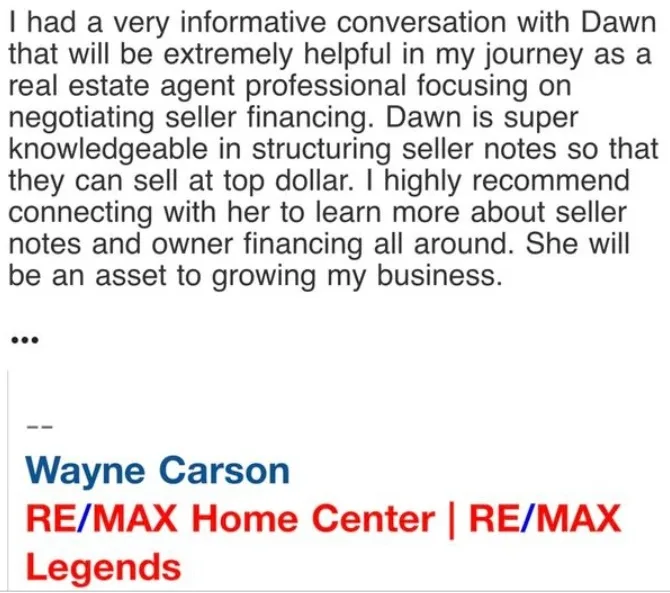

Dawn — Senior Seller Finance Note Advisor & Analyst

Moxxie Asset Group · Ft. Lauderdale, FL

Quick Answers

- → Owner financing is a 250-year American tradition — neighbors financed neighbors' property long before banks, mortgage companies, or credit scores existed

- → Your note has a present lump-sum value today — not just a stream of future monthly payments

- → You can sell all or part of your note — a full sale for a clean exit, or a partial note purchase for cash now plus income later

- → Typical closing time: 3–5 weeks when all documents are received and title is clear

- → Free note review — no obligation → Request a FREE Note Review

Two hundred and fifty years ago, Americans declared independence from a system that told them they had no choices. That the way things were was the way things had to be.

Before banks existed. Before mortgage companies, loan officers, and credit scores — Americans were already buying and selling property using seller financed notes. A farmer selling land to a neighbor. A merchant carrying paper on a storefront. The seller became the bank. The buyer made payments. A promissory note documented the agreement.

Owner financing did not start in a real estate seminar. It started in 1776. Your seller financed mortgage note is part of a 250-year American tradition.

Owner Financing Is as American as July 4th

Seller financing has been the backbone of American real estate for as long as there has been American real estate. Long before Fannie Mae, before FHA loans, before credit bureaus and debt-to-income ratios — neighbors were financing each other's dreams on a handshake and a promissory note. The practice grew out of necessity and community trust, in a country where the nearest bank might be days away, if one existed at all.

It worked then. It works now. Today, thousands of seller financed notes are created every year across the United States. Texas alone creates more than 20,000 owner financed transactions annually. Florida, North Carolina, Georgia, Michigan, Oregon — every state has note holders quietly collecting payments on seller financed real estate deals they created, often years or even decades ago. If you signed the paperwork on one of these deals as the seller, you are carrying on a tradition older than the country's central banking system itself.

What has changed over 250 years is not the fundamental structure of a seller financed note — it is the options available to the person holding one. Today, note holders have access to something the farmers and merchants of 1776 never had: a professional market of buyers ready to purchase that note, in full or in part, for cash today. If you would like to understand the mechanics of that process in more detail, see our full guide on how to sell a mortgage note.

But Is Your Note Working for You Right Now?

Monthly payments arriving in your mailbox feel like income. And they are. But they are income on someone else's schedule. A fixed amount. A fixed date. For 10, 15, maybe 20 more years. That is not freedom. That is a very slow drip.

Your note is not just a stream of future payments. It is an asset with a present value that can be converted into a lump sum today — if you choose. Some note holders sell the entire note. Clean exit. Complete financial independence. Others prefer a partial note purchase — cash today, income tomorrow. The best of both worlds, structured so you receive a defined number of payments as a lump sum now while continuing to collect the remaining payment stream later.

Either way, the choice is yours. That is the point. That has always been the point — from the farmer carrying paper on a land sale in 1776 to the note holder deciding what to do with a seller financed mortgage today. The instrument has evolved. The freedom to decide what happens next has not.

Free — No Obligation

Ready to Find Out What Your Note Is Worth?

Our team reviews your note and responds within one business day — no fees, no pressure, no obligation.

Declare Your Own Financial Independence

The Founding Fathers decided that waiting was not an option. Neither should you — at least not without knowing all your options.

Find out what your note is actually worth in today's market. Not what the balance says. What someone would actually pay you for it today. That conversation costs nothing. And it might be the most important financial conversation you have this year.

Gather your mortgage or deed of trust (depending on your state) and reach out to our team for a free, no-obligation note review. We work with note holders across all 50 states — from South Florida to the Pacific Northwest. Whether you decide to sell the entire note, sell a portion of it, or simply hold onto it a little longer with a clearer picture of what it is worth, that decision should be yours to make with full information — not one made for you by circumstance.

Frequently Asked Questions

What is a seller financed mortgage note?

A seller financed mortgage note — also called an owner financed note or private mortgage note — is a legal agreement where the seller of a property acts as the lender. Instead of the buyer getting a bank loan, the seller carries the financing directly. The buyer makes regular payments to the seller, who holds a promissory note and a mortgage or deed of trust as security. Seller financing has been used in American real estate for over 250 years and continues to be common today — particularly for properties where conventional financing is difficult to obtain.

Can I sell my seller financed mortgage note for a lump sum?

Yes. You can sell your seller financed mortgage note to a professional note buyer for a lump sum of cash today. You do not have to wait years for all the payments to come in. Note buyers evaluate your note based on the remaining balance, interest rate, payment history, borrower creditworthiness, and the property securing the note. The process typically takes 3–5 weeks when all documents are received and title is clear. You can also choose a partial note purchase — selling a defined number of payments for a lump sum today while keeping the rest of the payment stream.

What documents do I need to sell my mortgage note?

At a minimum, gather your mortgage or deed of trust (depending on your state), the original promissory note, the closing or settlement statement from when the note was created, and a record of the borrower's payment history. Having these documents organized and ready speeds up the evaluation and closing process. Our team can often begin a free note review with partial information and guide you on what else may be needed.