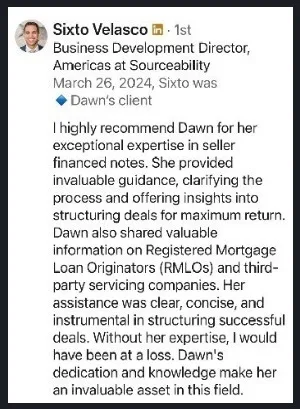

Dawn — Senior Seller Finance Note Advisor & Analyst

Moxxie Asset Group · Ft. Lauderdale, FL

Quick Answers

- → Your note's value is not fixed at closing — there are specific steps you can take before and after to move the number up

- → Biggest at-closing move: involving a licensed RMLO in origination — typically paid by the buyer, not you

- → Biggest post-closing move: track every payment meticulously — 12+ months of on-time history directly increases your offer

- → Know before you need to sell — note holders who know their note's value have leverage; those who need cash fast lose it

- → Free professional note evaluation — no fees, no obligation → Request a FREE Note Review

Most seller financed mortgage note holders assume that once the deal is done, the value of their note is locked in forever.

It is not.

There are things you can do right now that directly affect what your note is worth. Some should have been done at closing. Others can still be done today. Either way, the time to act is before you need to sell — not after.

What Should Have Happened at Closing

The single most valuable thing a seller financed mortgage note holder can do happens before the ink is dry.

Hire a Residential Mortgage Loan Originator — commonly known as an RMLO.

Most note holders have never heard of one. And that gap is costing them.

An RMLO is a licensed mortgage professional who handles the origination of your seller financed note the same way a bank would handle a traditional mortgage. Here is what they do for you: they pull your buyer's credit report, analyze your buyer's debt-to-income ratio to confirm they can actually afford the payment, and prepare proper loan documentation — all in compliance with federal lending laws that most private note holders do not even know apply to them.

Here is what surprises most note holders: the cost of the RMLO is typically paid by the buyer at closing — not you. You get professional-grade documentation and a properly originated note at no cost to yourself.

A note originated with RMLO involvement is significantly more valuable than one created on a handshake. Note buyers know the difference immediately.

If you did not use an RMLO when you created your note, you are not alone — most private note holders do not. But if you ever create another note, an RMLO should be your first call. Our team can point you in the right direction. Just reach out.

Free — No Obligation

Ready to Find Out What Your Note Is Worth?

Our team reviews your note and responds within one business day — no fees, no pressure, no obligation.

Get a Lender's Title Policy at Closing

This one cannot be fixed after the fact — but it is critical to understand for any future notes you create.

A lender's title policy protects your interest in the property securing your note. If there are any title defects — liens, ownership disputes, errors in the public record — a lender's title policy covers you. This is different from the buyer's title policy, which protects the buyer's ownership interest. You need your own separate lender's title policy to protect your position as the note holder.

A lender's title policy must be purchased at closing. It cannot be obtained after the fact. If you did not get one when you created your note, you may have exposure you are not aware of — which is one of the reasons a professional note evaluation is so important. It helps you understand exactly what you are holding and any gaps in your documentation. For any future seller financed notes you create, a lender's title policy is non-negotiable.

What You Can Still Do After Closing

Did not use an RMLO? Did not get a lender's title policy? It is not too late to improve your note's value. Here is what you can do right now.

Get Your Documentation in Order

Your original promissory note is a negotiable instrument. Whoever physically holds that original wet-ink document has legal rights to the payments. Not a copy. Not a scan. The original.

Locate your original promissory note right now. If you cannot find it, you have a serious problem that needs to be addressed immediately. Once you find it, store it in a fireproof safe or a safe deposit box at your bank. Your mortgage or deed of trust (depending on your state) is recorded at the county and can be replaced. Your original promissory note cannot.

While you are at it, gather every piece of documentation related to your note: the mortgage or deed of trust, the closing disclosure, any correspondence with your buyer, and the original purchase contract. Organize it all in one place. Complete documentation directly increases your note's value — every missing piece tells the market there is risk, and the market prices that risk with a discount out of your pocket. See the full documents checklist for everything you should have on hand.

Track Your Payment History

Every on-time payment your buyer makes is building your note's value. Payment history is one of the most important factors in how your note is priced by any mortgage note buyer.

Keep a meticulous record of every payment received: date, amount, method, running balance. If you are not already doing this, start today. A note with 12 months of documented, clean payment history is worth more than a brand new note. A note with 24 months of clean history is worth even more. Every month of on-time payments is adding value to what you are holding.

Know What Your Buyer's Credit Looks Like Today

As the lender on your seller financed note, you have the right to pull your buyer's credit at any time — just like any other lender would. Most note holders never do this. They assume no news is good news as long as the payments keep coming. But payments coming in and your buyer's creditworthiness are two completely different things.

Your buyer could be carrying significant new debt. Their credit score could have dropped dramatically since closing. You would never know unless you pulled it. If their credit has declined since closing, that is something you need to know about — especially if you are considering selling your note. Note buyers will pull it and price accordingly. You should know what they are going to find before they find it. If their credit has improved since closing, that is a positive development that directly increases your note's value. Document it.

Know What the Property Is Worth Today

The property securing your note is your collateral. Its current value directly affects your note's risk profile and therefore its market value. Property values change. In some markets they have risen significantly. In others they have declined. An updated appraisal or current market analysis gives you a clear picture of the equity cushion in your note right now.

More equity means less risk for a mortgage note buyer. Less risk means better pricing for you. A declining property value is something you need to know about before a note buyer finds it. Get ahead of it.

The Most Important Thing You Can Do Right Now

Everything above improves your note's value. But none of it matters if you do not know where your note stands today.

The most important step is getting a professional note evaluation before you need to sell. Not when you need to sell. Before.

When note holders call us in a hurry — facing a medical bill, a business opportunity, a life event — they have no leverage. They take whatever number they are offered because they need cash now. Note holders who know exactly what their note is worth have all the leverage. They know when an offer is fair. They know what to negotiate. They know their options.

That is exactly what Moxxie Asset Group provides. Our team reviews your note — whether you are ready to sell or just want to know where you stand — and gives you an honest assessment with no pressure to move forward. If you want to understand how selling a mortgage note works before you request a review, start there.

Frequently Asked Questions

What is the single most important thing I can do to increase my note's value?

The single most valuable step happens before or at closing — involving a licensed Residential Mortgage Loan Originator (RMLO) in the origination of your note. An RMLO pulls the buyer's credit, analyzes their debt-to-income ratio, and prepares proper loan documentation in compliance with federal lending laws. Notes originated with RMLO involvement are significantly more marketable and command better pricing from note buyers. The cost is typically paid by the buyer at closing, not you.

Can I still increase my note's value after closing if I didn't use an RMLO?

Yes. While some steps — like obtaining a lender's title policy — must happen at closing, there is still a lot you can do after the fact. Locate and secure your original promissory note and all closing documents. Build a meticulous payment history record with dates, amounts, and running balance. Periodically pull your buyer's credit. And get an updated property valuation to know the current loan-to-value ratio. Each of these steps directly affects what a mortgage note buyer will offer you.

How does payment history affect what my mortgage note is worth?

Payment history is one of the most important factors in how a note is priced. A note with 12 months of documented on-time payments is worth more than a brand new note. A note with 24 months of clean history is worth even more. Every month of consistent, on-time payments adds value to what you are holding. Keep a meticulous record of every payment received — date, amount, method, and running balance — and have that documentation ready when you request a note review.