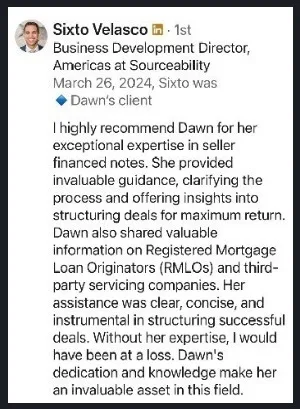

Dawn — Senior Seller Finance Note Advisor & Analyst

Moxxie Asset Group · Ft. Lauderdale, FL

Quick Answers

- → The process has 5 steps — initial evaluation, your decision to move forward, due diligence, final offer, and closing

- → Typical timeline: 3–5 weeks when all documents are received and title is clear

- → No obligation at any step — you can walk away after the ballpark offer or after the final offer

- → It starts with a free note evaluation — no cost, no obligation, just a preliminary number

- → Free professional note evaluation — no fees, no obligation → Request a FREE Note Review

Most seller financed mortgage note holders who are thinking about selling never start the conversation.

Not because they do not want to — because they do not know what is involved. The process feels mysterious, complicated, full of unknowns.

It is not. Selling a seller financed mortgage note is a straightforward process when you understand what is happening at each step and why. This post walks you through exactly what to expect from the first conversation to the day you get paid.

Step One — The Initial Note Evaluation

The process starts with a conversation. You share the basic details of your note with a note advisor — the balance owed, the interest rate, the remaining term, the property address, basic information about your buyer, how long they have been paying and whether payments have been on time.

Based on that information, the note advisor gives you a preliminary ballpark offer. This is not a final number — it is an educated estimate based on what you have shared, before anyone has verified anything. Think of it as a starting point. A way to know whether the conversation is worth continuing before anyone invests significant time or money.

At Moxxie Asset Group this initial evaluation is completely free. No cost. No obligation. No pressure to move forward.

Step Two — You Decide Whether To Move Forward

Free — No Obligation

Ready to Find Out What Your Note Is Worth?

Our team reviews your note and responds within one business day — no fees, no pressure, no obligation.

Once you have a ballpark number you decide whether it works for you.

If the number is not in the range you were hoping for, the conversation ends there. No harm done. You walk away with a better understanding of what your note is worth and why.

If the number is in the right range and you want to move forward, you sign a contract and give the note advisor permission to begin the due diligence process. Due diligence is the verification process — where the note buyer researches and confirms everything you shared in the initial evaluation.

Step Three — Due Diligence

Due diligence is simply the note buyer verifying that everything you told them about your note is accurate. They are confirming the details before they commit to a final purchase price. Here is exactly what due diligence involves:

- Pulling the borrower's credit report — the note buyer wants to know current creditworthiness

- Property appraisal or Broker's Price Opinion (BPO) — establishes current equity cushion

- Title search — checks for underlying liens, judgments, or title issues

- Verification of property taxes and homeowner's insurance

- Review of the closing statement or HUD-1 settlement statement

- Review of the original promissory note and mortgage or deed of trust

- Verification of payment history — this is where third-party note servicing is a significant advantage

- Verification of current note balance

Step Four — The Final Offer

Once due diligence is complete the note buyer presents a final purchase offer. This final number may differ from the initial ballpark offer. The ballpark offer was based on what you told them. The final offer is based on what they verified.

If due diligence findings match what you shared, the final offer will be close to the ballpark. If due diligence reveals issues — a credit drop, a title problem, delinquent taxes, missing documentation — the final offer reflects those findings.

You are never obligated to sell. If the final number does not work for you, the process ends there.

Step Five — Closing

If you accept the final offer, the note closes. Documents are prepared transferring your rights to the payments to the note buyer. You sign. The note buyer funds. You receive your payment — typically via wire transfer.

Your borrower is notified of the change and directed to send future payments to the note buyer or their servicing company. The terms of their loan do not change. Their payment amount stays the same. Their interest rate stays the same. Only the address they send the payment to changes.

How Long Does the Whole Process Take?

From initial conversation to funded closing, after the buyer has received all documentation from you, the process typically takes 3–5 weeks when all documents are received and title is clear. The due diligence process — appraisal, title search, credit pull, document review — takes most of that time.

What Makes the Process Smooth

Note holders who have their documentation organized and accessible move through the process faster and with fewer surprises. Your original promissory note. Your closing statement. Your payment history. Gather your mortgage or deed of trust (depending on your state). The more organized and complete your documentation the smoother and faster the process.

Note holders who have used third-party servicing have a significant advantage — their payment history is already documented and verifiable. If you are not sure what you will need, see the full documents checklist before you get started.

If you would rather sell only a portion of your future payments instead of the entire note, a partial note purchase follows this same process and may be a better fit depending on your goals. And if you want the bigger picture before you start, our guide to selling a mortgage note is a good place to begin.

Frequently Asked Questions

How long does it take to sell a seller financed mortgage note?

The process typically takes 3–5 weeks when all documents are received and title is clear. The due diligence process — appraisal, title search, credit pull, and document review — takes most of that time. Once due diligence is complete and a final offer is accepted, closing can happen quickly. Note holders who have organized documentation and use third-party servicing move through the process faster.

Do I have to accept the final offer after due diligence?

No. You are never obligated to sell at any point in the process. If the final offer does not work for you after due diligence, you can walk away. The process is designed to give you complete information about what your note is worth before you make any commitment. Our team reviews your note at no cost and no obligation.

What documents do I need to sell my mortgage note?

At a minimum, gather your mortgage or deed of trust (depending on your state), the original promissory note, the closing or settlement statement from when the note was created, and a record of the borrower's payment history. Having these on hand speeds up the evaluation and closing process significantly.